HOOGWEGT: Global OutputStrong Despite COVID-19

Hoogwegt Horizon December article

Global milk production volumes in 2020 were more than enoughto fulfill demand as foodservice outlets closed and peopleworldwide turned almost entirely to retail food sources due torecurrent local and countrywide lockdowns. Now that COVID-19vaccines are beginning to be distributed throughout parts of theworld, foodservice demand could begin to recover in earnest inmid-2021. In the meantime, though, unstable demand will collidewith rising stockpiles of dairy products to weaken the milkproducing sector unless governments maintain subsidies.

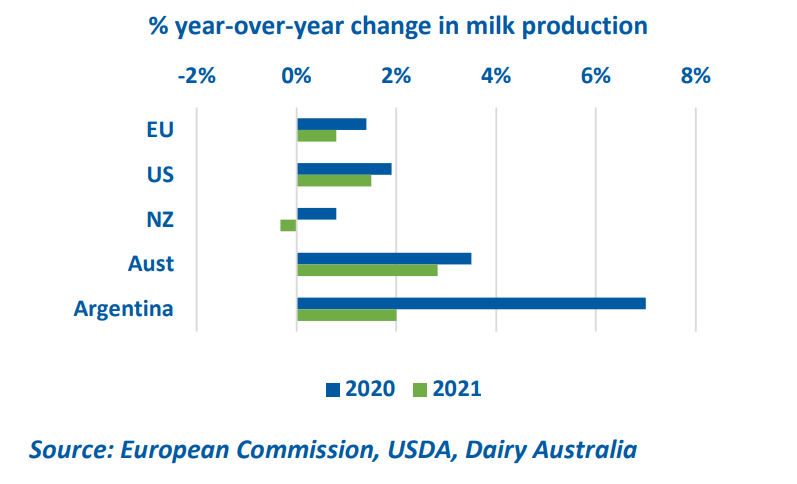

According to Italy’s CLAL, EU 2020 milk production throughSeptember—driven by a slowdown in culling and higher yields—increased 1.7% above the first nine months of 2019 beforetrailing off seasonally. For the year, the European Commission(EC) expects milk volumes to best last year by 1.4%. Following aninitial drop in prices last spring due to COVID-19, milk and dairyproduct prices have since remained stable or increased, aided inpart by the reopening of the Private Storage Aid (PSA) program.The EC projects year-over-year production growth next year toonly near 0.8% because the high growth rates of 2020 will behard to maintain as the world economy, weakened by thepandemic, struggles to recover.

Aid Drives U.S. Milk Output

In the United States, milk prices that surpassed $20/cwt. forsome producers through much of 2020 have driven milk outputhigher. For the year, total U.S. output will likely best 2019 levelsby 1.9%. So far this year, the United States has spent more than$5 billion to subsidize the dairy industry, providing $4 billion indirect payments to farms and the remainder to purchase food,including milk and cheese, to help the unemployed. U.S. output inthe first half of 2021 will depend on how quickly companies andgovernments can distribute vaccines and how robust demandrecovery is at foodservice. For now, USDA is predicting a 1.5%year-over-year increase in 2021 output.

In New Zealand, where the virus has not wreaked as much havocas it has in Europe and the United States, weather will once againbe the major factor affecting the outlook for milk production.New Zealand output passed the 2020-21 seasonal peak slightlyabove prior-year levels, but growth slowed after a strong start tospring. Looking ahead, a La Niña event could bring warmerweather to both islands, but heavy rainfall events are anticipatedin the north while the south should remain drier. Farm marginsare likely to be a little weaker than last year, with milk pricesprojected to finish near $7 (NZ) on a per kilogram of milk solidsbasis. USDA forecasts New Zealand milk production in 2021 todrop 0.3% below 2019 levels.

In Australia’s southern production regions, good pastures in earlyspring produced growth in milk collections, but gains stalledduring peak production months. Despite lower feed prices andimproved irrigation availability, year-over-year milk production isunlikely to grow in the first half of 2021 due to strong 2020comparisons. East coast fresh milk regions remain distressed,which will pull more milk from manufacturing. Dairy Australiaexpects milk collections for the 2020-21 season to grow 1-3%.

Milk production in Argentina is expected to advance at a muchslower rate in 2021, compared to this year, limited by weatherand eroding farm margins as inflation continues unabated. Theeffects of COVID-19 on domestic dairy demand pushed more milkinto driers in Argentina this year, while weaker milk collections insouthern Brazil could extend the country’s recent surge in wholemilk powder imports. USDA projects Argentina’s milk output willgrow 2% in 2021.

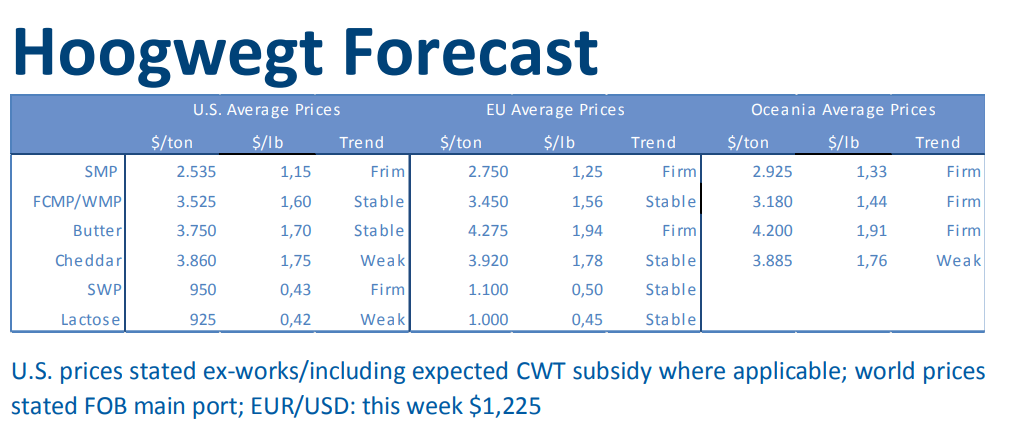

World Comment

EU milk exports has been less dominant in 2020 in comparison with the previousyears. Total production growth was also less than initially expected, and ended up in aminor and a bit disappointing growth. Global exports were relying much more on theUS and the Americas. US production growth was above 3% in November, which wasthe highest growth figure in many years. In Oceania we’ve seen a very strong seasonso far. But due to the exceptional strong season last year, we’ll hardly see any YoYgrowth. However, we can still conclude that Oceania managed to have a second strong season in a row.

On the demand side we’ve seen a very strong year from China. In October total imports already grew by 20% for powders, and 60% forbutter. Mexico has shown the weakest figures of the top 10 importers, and it’s still unknown how they will end the year. We do havesignals of stronger imports towards the end of 2020. If Mexico does manage to improve imports, we might see higher import figures of thetop 10 importers than last year.

Demand to Hinge on Economic Recovery

The outlook for the 2021 global economy remains hopeful asgovernments roll out Covid-19 vaccines. For this year, theOrganization for Economic Development and Cooperation (OECD)predicts the global economy will decline by 4.2%, an upwardrevision from September’s forecast for a 4.5% drop. OECD thinksthe world economy could recover to pre-pandemic levels by theend of next year, assuming countries maintain fiscal stimulus,including support for the world’s most vulnerable populations.

OECD expects China to be the only major country to showeconomic growth this year. Next year, China could account forone-third of the world’s economic growth, and a GlobalDatasurvey shows dairy demand remains strong in China, with 51% ofconsumers increasing fluid milk intake due to its health benefits.

As economies recover and COVID-19 infections subside, citizensworldwide could gain enough confidence to attend large events,dine-in at restaurants, and travel more and for farther distances.As this recovery takes place, dairy demand will increasingly shiftinto foodservice, and supply chains should return to their preCOVID balance soon thereafter.

However, vaccine deployment could take years in many of theworld’s developing countries, where economic recovery couldalso be delayed. Struggling economies in these regions as well asexchange rates will have a major bearing on global dairy trade in2021. According to Bloomberg, the median consensus forecastcalls for the euro to strengthen against the U.S. dollar next year,giving more of an edge to U.S. exporters in world markets.

Developed economies, where stocks of dairy products are large,have an opportunity to provide much needed aid and nutrition toless fortunate countries as they struggle to emerge from theworst pandemic in a century.