Agriculture, Including Dairy, Moves to Zero Emissions

May 2021 HoogWegt Horizon

Governments, entire industries, and companies continue to commit to net zero carbon emissions, and agriculture, including dairy, will be among those industries looking to adapt.

Carbon dioxide, methane, nitrous oxide, and fluorinated gasses are the primary greenhouse gasses (GHG). The dairy industry— from farm to table—emits all four, with carbon and methane being of greatest concern.

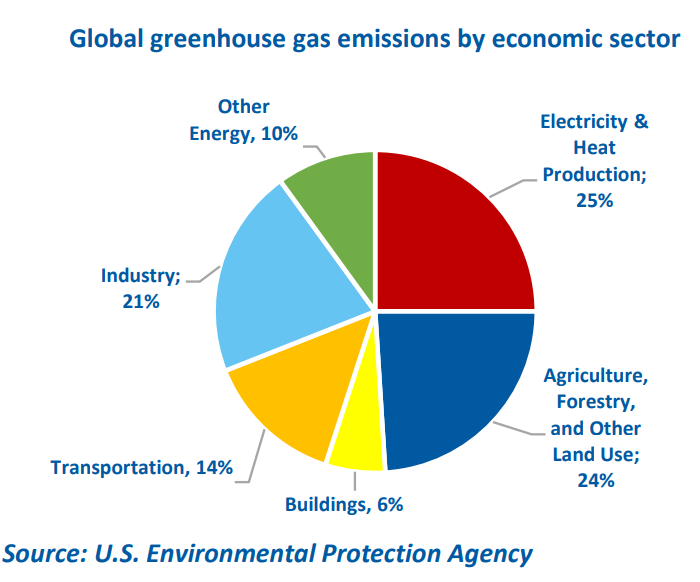

According to the U.S. Environmental Protection Agency (EPA), agriculture, forestry, and other land uses combined emit 24% of all global GHG, with agriculture and deforestation accounting for most of that. A study by the Food and Agricultural Organization shows that the global dairy sector contributes about 4% of all human-derived GHG emissions. USDA to Focus on Reducing Climate Change The European Union has proposed its Farm to Fork initiative, a cornerstone of the bloc’s larger Green Deal, to achieve net zero emissions from the food system by 2050. Target goals for 2030 include reducing use of pesticides by 50%, fertilizers by 20%, and antimicrobials by 50%, all while increasing land used for organic production to 25% of the total farmland. A recent USDA Economic Research Service study, however, showed that if adopted, targeted reductions would result in a 7- 12% decline in agricultural output and a 9% increase in world food prices by 2030. If these strategies were adopted globally, food prices would nearly double, according to the study.

The United States, following the Trump administration’s brief period of rolling back environmental restrictions, has rejoined the Paris Agreement and as such has recommitted to cutting GHG emissions in half by 2030. President Joe Biden has since said that the United States is now on a path to achieving net zero emissions no later than 2050.

The U.S. dairy industry has also committed to carbon neutrality by 2050, and the nation’s largest dairy cooperative, Dairy Farmers of America (DFA), has set goals to reduce both direct and value chain GHG emissions by 30% by 2030, from 2018 levels. DFA hopes to achieve these goals by supporting advances in feed efficiency, herd nutrition and feed additives designed to reduce emissions; renewable energies; anaerobic digesters; emissions capture through healthy soils and crops; transportation and hauling efficiencies; and research into green technologies.

In 2019, New Zealand also passed climate legislation that sets a target for net zero carbon emissions by 2050 and set up a Climate Change Commission to determine how to achieve that goal. New Zealand is also committed to reducing biogenic methane emissions, which account for about 43% of the country’s total GHG emissions, and about 70% stems from agriculture. New Zealand has set goals to reduce methane emissions by 10% by 2030 and between 24% and 47% by 2050, compared with 2017 levels. Unlike carbon dioxide or methane release from fossil fuels, biogenic methane emissions, if stable, will not increase global warming, the country said.

Consumer polls continue to show people want governments, and food producers and manufacturers to do more to achieve a sustainable food system, a fact not lost on some of the world’s largest food companies. For example, Nestlé, Danone, General Mills, and others have also committed to net zero emissions by 2050, which will further require producers to comply.

World Comment

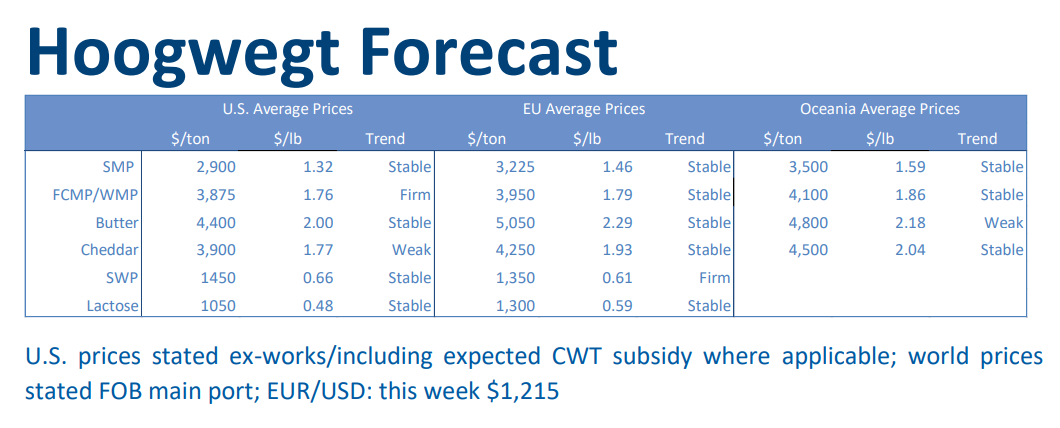

Global Milk Production is developing positively. During the first quarter year-on-year growth was minimal as higher production in the US was compensated with a lower production in the EU, which was suffering from unfavorable weather conditions. However all signs are on green for good milk production in the April-June period, as well New Zealand is having a strong end of their season. Milk production is expected to remain good for the remainder of 2021. New Zealand manufacturers have forecasted high milk prices for the new season and in South-America milk is valorizing well above crop. On the demand side we see continuing good dairy consumption in US and Europe and although COVID-19 influence is expected to become less in the second half of 2021, no significant change is forecasted. China continues to import strongly, mainly (NZ) WMP and SMP, although in the last week we saw some signs that the increases are leveling off. Middle-East and African demand has been behind on previous years, likely due to high prices, but South-East Asia has been showing positive growth. All in all we see dairy commodities currently priced at the high end of the price range. We could see some corrections in coming months, but general outlook remains fairly optimistic for the rest of 2021.

Early Adopters Will Likely Gain Market Share

Achieving net zero emissions by 2050 could prove daunting, requiring a concerted effort globally and among industries.

Moreover, feeding the world’s population of more than 9 billion people in 2050 will require rapid adoption of new food production and processing technologies. In the meantime, governments are struggling to balance the demands of competing sectors. Last year, to offset emissions generated from building 75,000 new homes, the Netherlands proposed a temporary limit on the addition of supplemental protein in dairy concentrates to reduce nitrogen emissions. Farmer opposition and a shortage of protein-rich pasture grass forced the Netherlands to scrap the proposal.

Moreover, new environmental policies have contributed to a slowdown in growth in most of the world’s milk-producing regions, a trend that will likely accelerate. The European Commission (EC) forecasts that average annual milk production growth through 2030 will drop to 0.6% for the European Union, 0.8% for the United States, and 0.4% for New Zealand, compared to 1.6%, 1.5%, and 2.5%, respectively, between 2010 and 2020. However, the EC notes that dairy product growth could outpace gains in total milk production through advances in genetics and feed strategies that promote higher milk components.

In the short-term, business and investments could continue to flow to low-cost milk producing regions as well as to low-cost product manufacturers regardless of emissions. But longer term, as milk production shifts to areas where both producers and processors adopt green technologies and practices the quickest, while keeping milk production growth robust, investments in dairy product processing will follow. As with any new technology, the earliest adopters stand to gain the most, but this transition could prove both costly and difficult.