Climate Change Could Limit Expansion

The new decade will usher in world milk prices that are substantially higher than a year ago, and that could accelerate milk production growth, particularly in the Northern Hemisphere,as the year unfolds. At the same time, though, worldwide concerns over climate change and the resulting environmental pressures in major milk‐producing regions could limit milk production expansion going forward. With U.S. cheese and whey demand still expanding, a large share of next year’s additional milk will likely head to cheese vats, with some milk sent to driers as stockpiles of skim milk powder (SMP) dwindle.

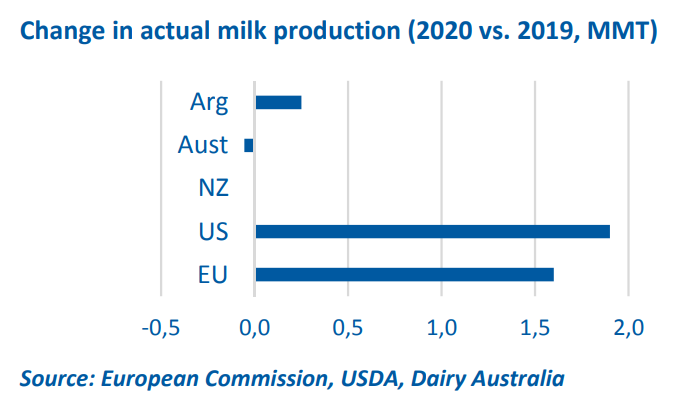

The world’s largest milk‐producing region continues to produce ever‐larger volumes of milk. According to the European Commission, year‐over‐year EU milk collections are expected to grow 0.5% in 2019 to 158 million metric tons (MMT), followed by a gain of 1% in 2020. However, mounting environmental pressures, which have spurred protests in Ireland and France,threaten to limit expansion going forward. Over the past two years, EU milk output has grown more slowly than demand,helping to exhaust the trading bloc’s once‐burdensome Intervention SMP stocks. While EU output of cheese will expand in 2020, production could also shift into milk powders to help meet growing global demand.

U.S. farm financials improve In the United States, following years of low milk prices, year‐over‐year milk production in the first 10 months of this year was up less than 0.3%, compared to the comparable period in 2018.Given significantly higher fourth‐quarter milk prices, in addition to aid provided by the government to offset markets lost in the U.S.‐China trade war, U.S. dairy producers have started to shore up their financials. USDA projects full‐year 2019 U.S. milk production to exceed 2018 levels by less than 0.2%, while output next year will grow by 1.7% to 101.6 MMT. With younger cows entering the herd and ongoing improvements in genetics and technologies, both output per cow and the components in the milk will continue to climb, allowing manufacturers to produce more products from a smaller milk herd. This could be a critical factor moving forward as regions strive to remain competitive amid growing concerns over climate change

Production gains in the Southern Hemisphere next year will not be as significant. New Zealand’s 2019‐20 milk production has peaked and is now slightly below prior‐year levels. New Zealand’s National Institute of Water and Atmospheric Research predicts that the country’s weather will likely be warmer and drier than normal in coming months, yet early 2020 production is expected to improve on 2019’s sharp declines. Farm margins are also expected to recover along with milk prices. However, as banks maintain firm pressure on farmers to reduce debt exposures and environmental pressures increase, farm operating costs will continue to rise, limiting prospects for expansion. Assuming normal weather, USDA expects 2020 calendar‐year milk production in New Zealand to be flat compared with 2019.

Milk production in Australia continues to contract, due to inconsistent pasture conditions, elevated feed prices, and exorbitant irrigation water costs. East coast regions with heavy fluid consumption continue to suffer from drought, which means more milk will be pulled north further depleting export supplies.Dairy Australia expects 2019‐20 milk collections to fall 3‐5%below the previous season due to continued drought.

Stable weather and improved margins have supported a small recovery in Argentina’s milk collections since mid‐2019. However,the dairy sector faces further uncertainty in 2020 with the new government yet to form major policies to stabilize the peso and rein in consumer inflation. USDA expects Argentine milk output to reflect favorable margins and grow by 2.3% in 2020.

World Comment

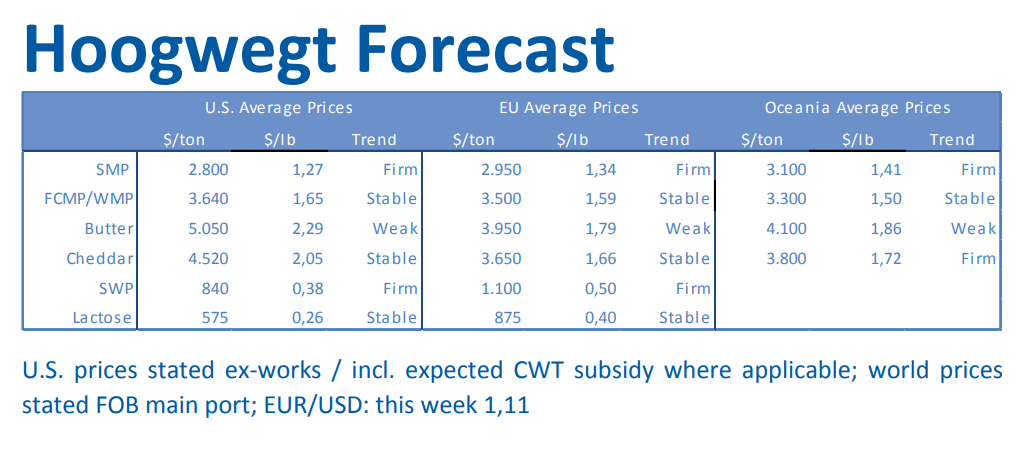

SMP prices are still firm, but in the last weeks prices have not increased as steeply asin the period before. Most buyers have reluctantly purchased up to about USD3000/mt CFr and now take a breath. However, assuming import demand will not drastically drop as a consequence of these, relative, high prices, it seems highly unlikely prices will fall back anytime soon. Flush in the Northern Hemisphere could give some downward pressure, but that is still a few months away. WMP market in EU is quiet and as well last Gdt didn’t show the increase that many expected. Milk valorization is still in favor SMP/Butterfat over WMP, but as both Oceania and European butterfat prices are under pressure some manufacturers might want to avoid building stocks of butter or AMF. Cheese market in both US and EU is stable at healthy levels. December could be a month with little movement on prices due to the Holiday Season, but in general limited growth in milk supply does not give reason for a fundamental bearish view.

Global Demand Likely to Remain Robust

Global demand for most dairy products remains robust, but adown turn in the world economy would choke off a share of dairy demand. According to a recent outlook from the World Trade Organization, the state of the world economy looks precarious and the pace of global economic activity remains weak. While geopolitical tensions have taken a toll on business confidence,investment decisions, and global trade, a loosening of monetary policy has thus far cushioned the impact.

The U.S.‐China trade war, in particular, has undercut the world economy and shifted trade alliances. Since the trade war began in July 2018, China has increasingly looked to Oceania and the European Union to fill its dairy product needs. Recent trade agreements have also shifted trade patterns, with the European Union gaining a greater foothold in many key U.S. dairy markets,including China, Mexico, South Korea, and Japan. Export supplies from New Zealand, meanwhile, have barely kept up with China’s growing appetite for milk powders.China’s ongoing epidemic of African swine fever and the proliferation of plant‐based dairy alternatives have likely skimmed off some dairy demand. However, all of the world’s largest dairy exporters saw business increase, for the most part,in 2019. For the first nine months of the year, year‐over‐year EU exports to countries outside the trading bloc soared, with butter and SMP both up 28% and cheese exports up 4%. Likewise, New Zealand exports of whole milk powder were 15% higher than the same period a year earlier, with SMP exports up nearly 13%, and cheese up 4.3%. U.S. exports of cheese were 3.6% higher through September, but SMP/nonfat dry milk exports fell 10.9%.Barring a downturn in the global economy, world dairy exports should continue their trend higher well into the new year, helping to spur additional milk production. If environmental pressures mount for dairy producers, limiting milk production growth,availability of export supplies would also be affected.