GIs Protect Regions Often at Others’ Expens

Food manufacturers have been protecting their products for centuries through trademarks and patents, but the use of geographical indications (GIs)—a lesser used way to protect regional products—is spreading. Since 1991, the European Union has been applying its system of GIs within the EU trading bloc, but in recent years, the European Commission has been working to globalize that strategy by including GI protections in trade agreements.

According to the World Intellectual Property Organization (WIPO), GIs are “signs” used on products that originate from a specific geographical region and possess qualities, a reputation, or a manufacturing process attributed to that place of origin. “There is a clear link between the product and its original place of production,” WIPO states.

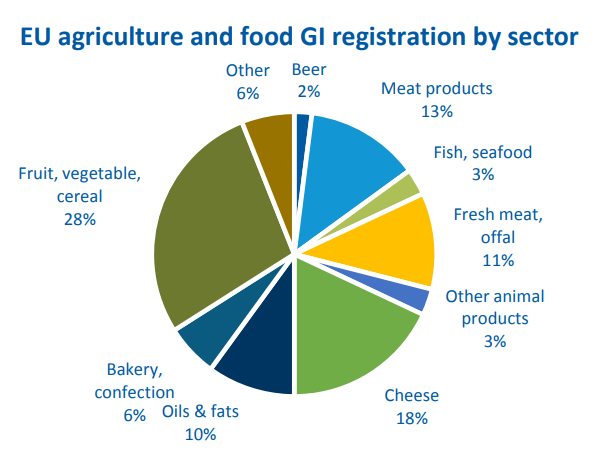

The Agreement on Trade‐Related Aspects of Intellectual Property Rights (TRIPS), an international agreement between members of the World Trade Organization, grants GI protections. Use of GIs is most widespread in the wine industry and practiced mainly by the European Union, United States, Australia, and New Zealand. The European Union has been most aggressive in implementing GIs. More than 3,300 food, wine, and spirt products produced in the European Union have a GI designation.

Protecting Generic Cheese Names In dairy,

while GI protections are prominent for EU cheeses, they could potentially affect other categories, such as Greek yogurt. The European Union has sought GI protection for Parmesan, Feta, Fontina, Mozzarella, and other cheeses. Grana, Havarti, and Pecorino, by contrast, are still considered generic cheese names. In June, the European Union contemplated approval of a controversial Danish application for Havarti. Currently, several countries outside of Denmark make the bulk of Havarti, which fails GI standards for several reasons, including no association with a specific region. The addition of a regional qualifier like “Danish Havarti” could be a candidate for GI protection. Attempts like these to protect generic names could spread to cheeses like Gouda and Edam.

The use of GIs has been expanding. The European Union has ratified trade agreements with Mexico, Canada, and Japan, all of which include GI protections for certain cheeses. Negotiations are also progressing with New Zealand, Australia, and MERCOSUR. For now, all of these agreements contain GI protections for cheeses. EU and U.S. cheese makers continue to make and sell competitive products to GI‐protected cheeses with equivalent quality for a lower cost. As more GI protections are included in trade agreements, it could become more difficult for these cheese makers to sell their products in some markets, but GIs only apply to single products, not product blends—a notable weakness in the protection.

For countries, regions, manufacturers, and rural communities, the purpose of protecting products with GIs is to create origin‐ labeled niche markets in an effort to expand demand for these products by claiming originality. Attempts to protect dairy products, especially generic cheese types, by implying non‐GI cheeses with similar names are imitations, continues to be contentious within the European Union and in the United States and New Zealand. The trend toward an ever‐increasing number of GI protections will likely continue, but not without strong opposition. Moreover, the proliferation of GIs for commodity cheese could eventually work against those seeking protection if GIs become meaningless to consumers.

World Comment

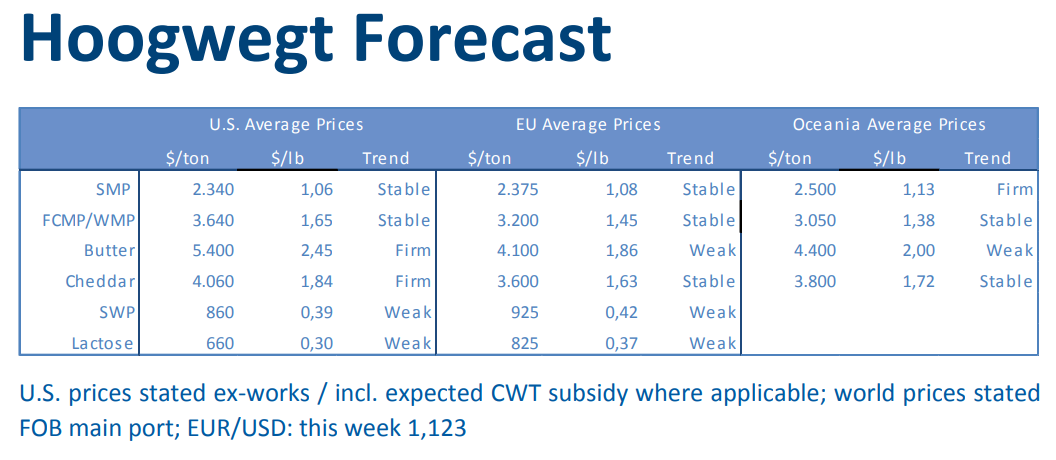

Global milk production is not convincing and only showing minimal increases. As well for the remainder of 2019 no significant increase is expected in any of the major milk producing regions. With steady demand for fresh products and increased quantities of milk flowing to cheese, production of commodity milk powders is stable at best. Longer term trends for import demand for commodity milk powders show a steady growth of 2 – 2.5%. With European Intervention SMP stocks disappearing, one can foresee a shortage in the coming months. For now most buyers are not panicking and only reluctantly accept today’s prices. With the SMP price trend already up since April of 2018 it is uncertain if buyers have filled their pipelines above average. WMP prices have stabilized after approximately 3 months of softening prices. Although demand is still limited, we will have again an interesting period ahead of us where the question again will be if demand from China will be enough to absorb the available volumes from New Zealand during their peak in production. As Chinese New Year is early this year, increased demand is expected to start a bit earlier as well, likely partly already before the reduced import duty period that starts January 1, 2020 again. SWP and other whey derivatives are still weak and not expected to recover before the Asian Swine Fever is under control.

GIs Being Used as Non‐Tariff Trade Barriers

GI protections can help consumers appreciate how traditional and regional influences from climate, the manufacturing process, and soils impart flavor and quality attributes to a given product. However, some countries are using GIs as non‐tariff trade barriers for commodity products to provide a competitive advantage into lucrative markets. How successful these types of protections might be is uncertain given challenges from other manufacturers that can provide high‐quality, low‐cost modifications to work around these barriers.

Those opposed to GI protections for generic dairy product names can fight the policy, try to develop their own protections, or work around GIs. The U.S. dairy industry continues to officially fight the policy, while the Danes have developed their own stance using regional qualifiers, such as “Danish White Cheese,” to offset the impact from GI protection for Feta originating from Greece only. Others are working around the protections by making blends. Packaged, shredded pizza cheese blends, for instance, often contain Mozzarella and Parmesan but would not violate GI protection. The Danish tactic of working around GIs appears to be more successful than the U.S. stance. While some EU GIs have proven successful, U.S. exports of cheese have not yet been harmed by GI protections issued to EU cheesemakers.

The largest fight for GI protection could play out in the United States if agriculture is brought under the umbrella of EU‐US trade discussions. The United States likely won’t permit wide sweeping GI application within its borders, but agriculture typically ranks low as a priority for U.S. trade negotiations. Thus, the question becomes whether the U.S. dairy industry would be able to create a sufficient roadblock if the European Union were to provide lucrative offers to other industries.

For now, GIs are here to stay, but how capable manufacturers are in working around them will determine whether GIs can provide a sustainable competitive advantage for EU manufacturers.