HoogWegt: Huge Potential inSub-Saharan Africa

HoogWegt Horizon March 2021

Sub-Saharan Africa is comprised of 46 countries and 1.1 billionpeople. The region had the world’s fastest population growthbetween 2000 and 2020. It is also one of the world’s mostimpoverished regions, with 2019 gross domestic product (GDP)per capita of just $1,596 (U.S.), virtually changed over the pastdecade, according to the World Bank. The region’s average GDPper capita is only 20% of the MENA region’s average and 14% ofEast Asia’s. Sub-Saharan economies are highly dependent onnatural resources, primarily crude oil, minerals and metals.

A number of countries in the region have dairy industries thatcombined produced an estimated 35 billion kilograms (77 billionpounds) of milk in 2019, according to the Food and AgricultureOrganization (FAO). This milk fills a major portion of the region’sdairy consumption. Sub-Saharan Africa’s dairy industry continuesto develop slowly, with significant input from major foodcompanies and foreign dairy industries. However, the region’sreliance on imports is expected to grow as consumption expands.

The region represented around 6% of global dairy trade(measured in milk solids equivalent) in 2020, with importsdominated by milk powders and small volumes of cheese andbutterfat. Dairy import volumes, which have varied over time andare sensitive to fluctuations in commodity prices, have grown byan average of 2.5% per year over the past decade, helped byproduct innovation and portion size that has improved accessand affordability within the region.

Fat-Filled Products Substituting for WMP

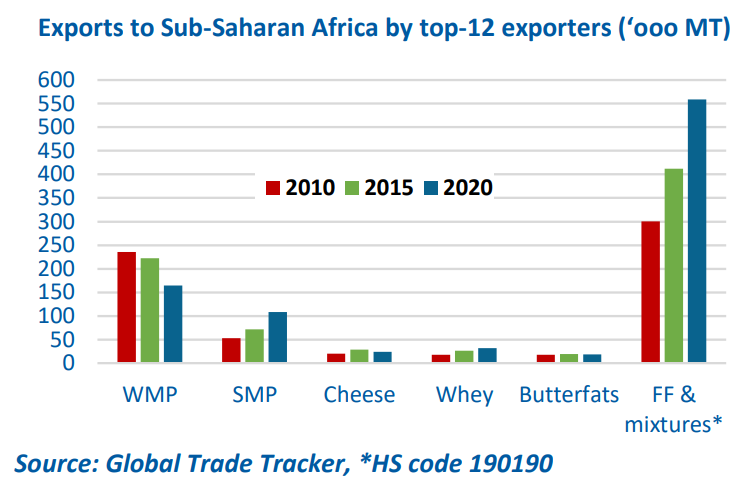

The development of skim milk powder (SMP) trade has beenslow, and over time, fat-filled milk products have substituted forwhole milk powder (WMP) purchases. Trade in fat-filled milkproducts has grown more than 6% per year over the past fiveyears, while trade in WMP declined by roughly 25%, due to thecost advantages vegetable oils have had over butterfat.

In late 2019, WMP imports to the region staged a partial recoverydue to attractive prices and improved economic conditions formajor importing countries, but the small import volumes ofcheese and butterfat products have been relatively static.Nigeria, the most populous nation in the region, with more than200 million people, is also the largest market in Sub-SaharanAfrica. Last year, the country imported about one-fourth of allmilk solids flowing into the region. Ethiopia, next in size with 112million people, relies primarily on its own production and importsonly small volumes of dairy products.

As one of the region’s more developed domestic dairy industries,South Africa produced 3.3 billion kilograms (7.3 billion pounds) ofmilk in 2019. The country is the region’s second largest importer,followed by Senegal (largest importer of fat-filled products),Ghana, and the Ivory Coast.

Projections for both population growth and dairy consumption inthe region are staggering. By 2050 the United Nations projectsthe region’s population will nearly double to 2.1 billion andaccount for 22% of the world’s people. Over the next 30 years,more than 50% of the world’s added population will live in SubSaharan Africa. As household incomes rise, and a larger share ofpeople in the region become dairy consumers, the global dairyindustry will face one of its biggest supply challenges.

The African Continental Free Trade Area, an ambitious free tradeagreement covering the entire continent, took effect Jan. 1, 2021.While still early, the agreement will provide a framework forengagement of the continent in dairy trade.

World Comment

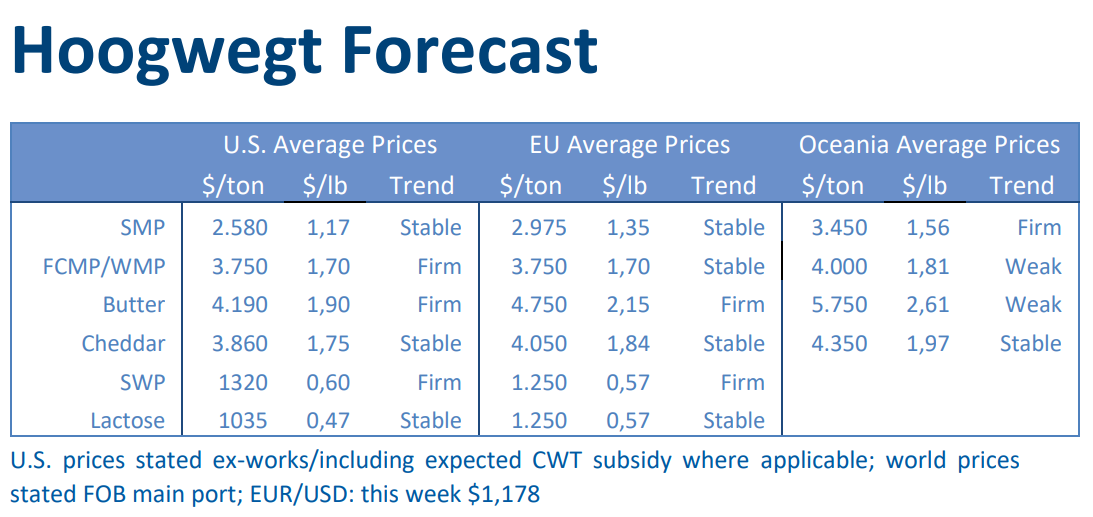

For the past weeks to months we’ve seen a steady and unbalanced world market. The EUis showing negative growth in January and February of about 0,4% and is only expected torecover in the peak months, April and May. In the US we experience a steady oversupplyof milk. However, the US is having difficulties with its export logistics and its ability toproduce medium heat SMP. These problems are the main reason behind the big price-gapbetween the EEX and CME. Without these production and logistical restrictions, the worldwould see a lot more US originated product and the EU would have been forced to adjust its pricing to the US. New Zealand is moving towardsits low season, and although Fonterra increased the volumes on GDT, we’re not expecting any major developments that will change theworld balance in the months to come. On the demand side key player is and will remain, China. Although supply growth in China acceleratingdue to large scale investments, it cannot keep up with the pace of the growing demand. Hence for 2021 we again expect growing importfigures from China.

Region Faces Rocky Road out of COVID-19Countries in Sub-Saharan Africa have managed to keep COVID-19cases relatively low, but the global effect of the pandemic has hitthe region hard. For the first time in 25 years, the region wentinto an economic recession in 2020. The International MonetaryFund (IMF) said the pandemic could set economic developmentof the region back by as many as five years.

Affordability will remain a challenge in coming years. For the firsttime in two decades, the share of population living in extremepoverty will increase due to the pandemic’s flow-on effects. Inaddition, reduced foreign financing flows from remittances,tourism, and foreign investment are more widely threateningbusinesses and employment.

Dairy shipments to the region slowed in late 2020 as majoreconomies reeled from a collapse in crude oil and othercommodity prices. Year-over-year WMP exports to the regionslowed to less than 5% growth in the second half of 2020 andlikely will come under further pressure from this year’s risingprices. SMP exports to the region fell 15% in the second half of2020 as prices increased. Before recovering late last year, exportsof fat-filled powders and mixtures also slowed as vegetable oilprices soared. Dairy exports to Nigeria and Angola, economieswith high exposure to crude oil, have posted the largest overallvolume declines.

Whether Sub-Saharan Africa will be able to continue to containCOVID-19 will be the major determinant in how fast the region’seconomies recover. Without large-scale humanitarianintervention and close integration between countries in theregion, current forecasts suggest that the slow rollout of vaccineswill prevent Sub-Saharan Africa from returning to normal mobilityuntil sometime well into 2023.