HoogWegt Horizon: COVID19 Snarls Global Supply Chains

HoogWegt Horizon on April 2020

The COVID19 global pandemic has disrupted dairy exports and supply chains throughout the world. Entire regions, countries,and cities have been locked down, causing wide scale closures of events, restaurants, businesses, and schools. Even in areas not officially locked down, governments have asked consumers to socially distance themselves from others and stay home. The ensuing panic has often resulted in a foodhoarding mentality that at times has given the false impression that milk and dairy products were in short supply.

The mass shutdown of food service in countries around the world has resulted in a back up of dairy products. During the worst of the pandemic, grocery stores in Europe and the United States sold out of milk and other dairy products, but retail sales have not been large enough to offset the steep losses in foodservice. Over the last decade, increasing sales at food service have driven both the growth in dairy product consumption and the recovery in prices in both Europe and the United States as consumers continued to spend an increasing share of their food budgets at restaurants. The U.S. food service sector typically accounts for 30% of all milk solids consumed in the United States annually.

Export supply chains stall While retail supply chains have remained relatively intact throughout major dairy exporting regions, international supply chains are more troublesome. Some products have been held up at ports for weeks, and many countries have closed their borders to people and, at times, goods. That could push even larger volumes of dairy products into warehouses and worsen what has already become a humanitarian crisis, especially if food can’t reach people in food deficit nations as the pandemic spreads.

The severe destruction of food service and export demand caused by COVID19 has sent milk and dairy product prices into a free fall. Prior to the worldwide spread of the contagion in March, the world’s milk supply was relatively balanced, but today, processors of storable dairy products have more milk than they can handle and not enough orders to continue business as usual. Until the food service sectors in Europe and the United States reopen, skim milk powder (SMP), processed cheeses, and butter will likely remain burdensome.

While the Northern Hemisphere works through its flush during the COVID19 crisis, New Zealand’s season has come to an early end, which will help mitigate supplies in the short term.Nonetheless, dairy producers worldwide are looking at much lower milk prices. To help keep these dairy producers in business,the United States and Europe have reopened their safety nets and started to implement strategies to reduce production.

In March, the European Union’s Intervention purchase program for SMP was reauthorized, with a fixed purchase price of€1,691/metric ton. Restrictions were also relaxed so that member states can offer up to €100,000 in 2020 to agricultural businesses that face difficulties as a result of COVID19. Farmers were also granted a one month extension to apply for aid under the bloc’s Common Agricultural Policy. Meanwhile, the United States passed legislation to provide $14 billion to replenish the Commodity Credit Corp. as well as $9.5 billion more for specialty crops and livestock, including dairy. While the United States eliminated its price support system in the 2014 farm bill, USDA still has a permanent appropriation under Section 32 to purchase the equivalent of 30% of annual customs receipts to support the farm sector. Last year, USDA purchased more than 19 million pounds of cheese and over 5 million units of fluid milk under this program for food aid and other uses. But whether this aid will reach dairy producers in time to stave off mass bankruptcies is uncertain.

World Comment

Since the global spread of Covid19 the overall global demand for dairy products has decreased. Demand fall out started in North Asia, followed by the rest of the world with a huge drop of demand in the food service industry. This drop in demand seems to be inevitable, the question remains, when will the supply side adapt to this decreased demand? US farm gate prices has dropped significantly and the financial burden will be expected in the months to come. However, milk production is not very likely to drop significantly given the governmental support. In the EU processors starting to adjust their prices of raw materials. Farm gate prices are still ok, general expectation is that this will decline into Q2. Expected effect on milk production is limited, since most of the farms aren’t taking output decreasing measures when the prices are falling. The current drought in the EU is likely to have a larger effect. Although farm gate prices in NZ are expected to be a lot lower the than the previous season, overall expectation is that prices will be sufficient for farmers. Latin America is expected to have a 2% increase in production as last year, although uncertainty is there because of the ongoing draught and the current economic circumstances.

Europe and the United States Grapple with Surplus

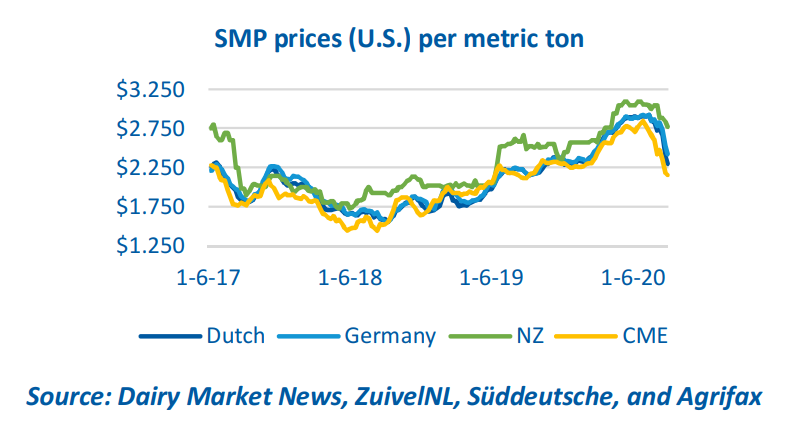

Nothing in recent history has hit the international dairy supply chain so forcefully and quickly as the COVID19 pandemic. The public health crisis, which engulfed the global dairy industry just when the long awaited milk price recovery was starting to take hold, has disrupted supply chains, temporarily putting demand and prices into a free fall. Between Jan. 31 and March 31, Dutch and German SMP prices lost more than 20% of their value and butter prices dropped 10%. Over the same period, U.S. Cheddar blocks, butter, and nonfat dry milk prices declined 30%.

In early April, Europe and the United States were contemplating ways to compensate dairy producers to slow output, while producers were being forced to dump surplus milk. Several regions of the United States reported high instances of dumped milk in early April. While that helped to solve the immediate crisis of not having enough plants to processes large volumes of milk as some plants shut down due to labor shortages or lack of orders, it could cause issues longer term if the dumped milk results in tighter supplies in months to come.

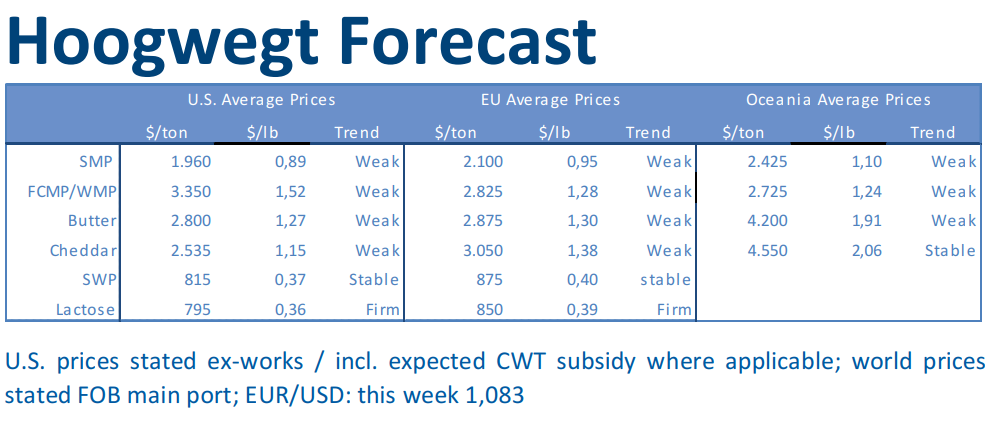

The vast oversupply of milk during the height of the pandemic inEurope and the United States has pushed global prices to levels not seen in years. U.S. farm gate prices are expected to fall to their lowest levels since 2012. However, if large numbers of the world’s dairy producers are unable to make it through this devastating period despite government support and food service recovers, the steep downturn in prices could be followed by a quick recovery.

Had COVID19 been contained to China, the global dairy industry could have escaped its current fate. In the first two months of this year at the height of China’s outbreak, China imported 62,950 metric tons (MT) of SMP after adjusting for leap day.While that was 26% less than the previous year, it was higher than the five year average of 58,850 MT for the same period—providing a glimpse into what the market could have been.