Hoogwegt Horizon feburary

Hard Brexit Would Disrupt Global Dairy Markets

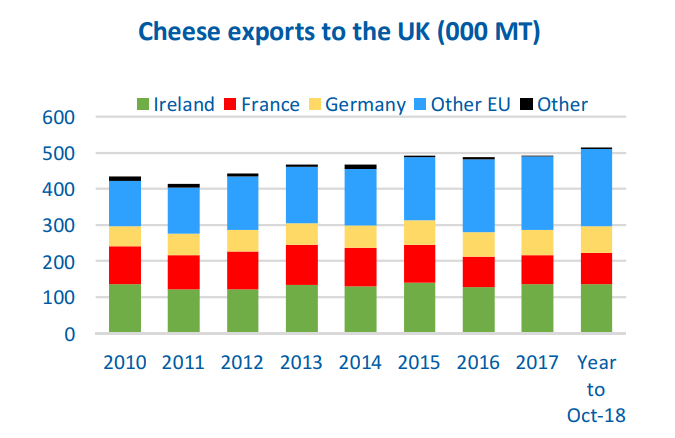

The unprecedented 2016 referendum calling for the United Kingdom (UK) to depart from the European Union, or “Brexit,” has not only created significant economic uncertainty and political divide but also threatens to disrupt global dairy trade. In late 2018, the UK and EU governments reached a complex Withdrawal Agreement regarding the Brexit withdrawal process, transition, and future relationships. Withdrawal affects a vast number of issues including trade, citizenship, labor, financial markets, and commerce. In January, the UK Parliament rejected a proposed agreement reached by Prime Minister Theresa May and the European government. That rejection and subsequent decisions by lawmakers have worsened the uncertainty. Substantial trade in cheese, butterfat, and bulk milk exists between EU members and the UK. If Brexit moves forward, the UK’s 66 million consumers would become the largest dairy market for the European Union, importing more than 500,000 metric tons (MT) of cheese, including diverse European specialty cheeses, and 77,000 MT of butter from EU member states. The UK in turn exports close to 190,000 MT of cheese and 40,000 MT of butter to the European Union and the rest of the world. Ireland is the largest supplier of cheese, mostly Cheddar, to the UK, accounting for about 50% of Ireland’s total cheese exports. Meanwhile, about 80% of raw milk output in Northern Ireland, which is part of the UK, is trucked into Ireland for processing, an economic activity crucial to both regions. The deep interdependence built between the UK and other EU members since the UK joined the European Union (effectively in 1973) goes far beyond trade in ingredients and finished goods; it affects a multitude of complex, highlyintegrated food supply chains moving in both directions across borders.

Deal or no-deal?

The Withdrawal Agreement allows the UK to remain in the European Economic Area, customs union, and single market. After a transition period ending Dec. 31, 2020, the UK and European Union could enter new trading arrangements, or the UK could seek other free or preferential trade deals. With the Brexit date of March 29, 2019, looming, time is quickly running out for the UK parliament to accept the Withdrawal Agreement and implement the necessary arrangements to prevent a “nodeal,” also called a “hard Brexit,” scenario.

A “nodeal” scenario could severely disrupt trade and damage the UK economy by impacting business investment, global financial markets, and consumer confidence. Many analysts think a nodeal Brexit would plunge the UK into recession, which would slow global economic growth, challenging dairy trade in many markets. Tariffs between the European Union and UK would immediately default to World Trade Organization (WTO) standard rates—35% for most products—and cause disruption in border inspections, adding significant cost and delay in the movement of products. This would sharply increase costs to UK food processors and consumers, reducing demand for imported dairy products, while making UK exports to the European Union uncompetitive. Several measures could mitigate the effects of abrupt change, such as delaying the Brexit date, agreeing to mutually impose low or no tariffs on trade between the UK and European Union, and economic stimulus to offset impacts on UK consumers and businesses. The UK is unlikely to seek to protect its dairy industry from imports, given its large dairy deficit and the current integration of crossborder food supply chains, but it could choose to economically support its dairy industry.

World Comment

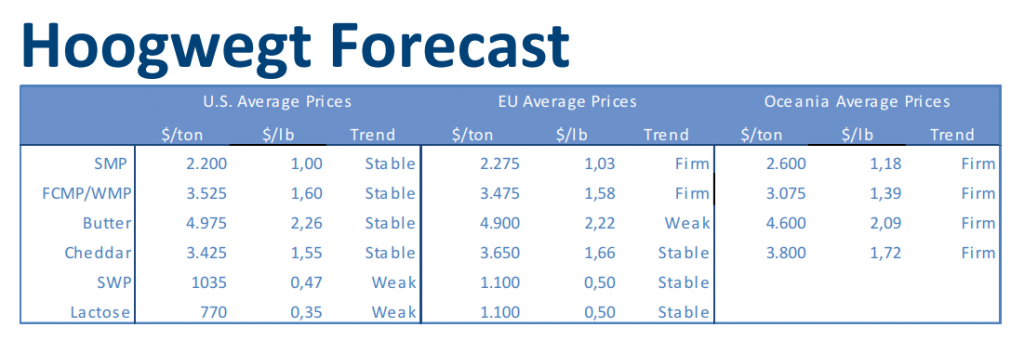

Growth of global milk production has dropped below 0% in the final months of 2018. Where USA and NZ are still showing a decent yearonyear growth, the other main milk producing regions are showing a strong decrease. After a very bullish start of 2019, the SMP/NFDM market had stabilized in the last weeks. Some improved availability in both New Zealand and Europe, combined with buyers taking a break had pushed prices a fraction down in both the physical and the futures market. However this week’s Gdt showed a surprising 4% increase in SMP prices and we can expect some new buying activity from Asian buyers returning from their Chinese New Year holiday next week. Latest USA statistics on NFDM/SMP are giving mixed signals; on one side we see very high stocks, but on the other side we see much lower production in 2018. As the combination butterfat / SMP is giving a better milk valorization, the production of WMP is relatively low and prices have been increasing steadily over the last months. If NZX futures are a good indicator, this is not expected to change. Demand from most importing countries is expected to be stable or firm with pipelines not overly well stocked. Normally, no major positive supply surprises can be expected from Oceania or SouthAmerica in their upcoming lowseason. For the coming 6 months it will be key to follow how milk production will develop in the upcoming flush season in the Northern Hemisphere.

Time Running Out for Highly Fluid Brexit Process

The Brexit situation remains highly fluid. As the departure date approaches, UK lawmakers appear to more clearly understand the risks posed by a “nodeal” scenario. That increasing realization could eventually drive compromise within the UK and between the European Union and UK on the terms of the Withdrawal Agreement—but time is short. Delaying departure until the UK has had time to resolve its position so it can avoid a nodeal scenario and allow time for negotiation with the European Union on the sticking points would be a highly desirable next step. A second public referendum to revisit the entire question of the UK leaving the European Union also remains an option. Uncertainty over Brexit and future access to the UK dairy market comes at a crucial time for EU markets, with the depletion of skim milk powder (SM) Intervention stocks and stabilization of butterfat markets after high prices damaged demand. Trade disruption caused by a hard Brexit and the risk of declining cheese demand in the UK could threaten global dairy market stability, especially if high volumes of milk are diverted into SMP and butter. Not that long ago, the loss of the Russian cheese market—about half the size of the UK market—triggered similar turmoil, from which the world market is just now emerging. Uncertainty has already affected behavior. Some UK cheese buyers are reportedly building stocks to avoid disruption. Ironically, as Brexit looms, dairy producer confidence is propelling milk production in Ireland and the UK. Yearoveryear output in Ireland climbed 23% in November and production is on track to expand 6% in 2019, according to Teagasc. In midJanuary, the UK set a daily record for the highest rolling annual production ever.