?HoogWegt: Australian Dairy Back from the Brink

HoogWegt Horizon August 2020

Since 2000, the year Australia’s dairy industry was fully deregulated, devastating droughts have taken a toll on the country’s milk production. Rolling annual milk collections peaked in 2002 at 11.3 billion liters (25.4 billion pounds) and they have been steadily contracting ever since. In 2019, extreme heat pushed milk collections 6.5% below 2018 to 8.6 billion liters (19.5 billion pounds), the lowest total since 1995. Of that, milk used in manufacturing fell to 6 billion liters (13.68 billion pounds).The challenge for Australian milk producers has intensified overtime. Unreliable rainfall has forced producers to improve on farmfeed security, lifting production costs and increasing farm management challenges. Fluctuating milk prices and weather have been the primary drivers of farm exits.

The loss of milk has been greatest in Northern Victoria, once the top milk producing region. The region, which is heavily reliant on irrigation, has tradable permanent water rights and temporary,or spot, water availability. Climate change has spurred the development of tougher environmental policies, which include government buying of water to sustain the health of river systems. Over time, competition for water, from both expanding environmental and horticulture uses, has driven up the price of water. In dry periods, including much of 2019, water can become cost prohibitive for many dairy producers. Future water policies and the cost of water create significant ongoing uncertainty forthe industry.

Increased Competition for Milk

The demise of Australia’s largest cooperative in 2016 altered the farm gate dynamic. More raw milk brokers have entered the market, in part to service former customers of the cooperative,resulting in more competition for milk. At the same time, a decline in milk collections has caused milk to increasingly shift into fresh milk for the domestic market and cheese.

Increased competition for milk, persistent import competition,and the high cost of upgrading small, underutilized plants has compelled processors to avoid further exposure to commodity price risk. As a result, processors are focusing on capturing value through producing branded and nutritional products. China is Australia’s largest export market by far, with infant formula accounting for nearly half the value of all dairy trade to China,according to Global Trade Tracker data.

Despite a decline in the overall pool of milk, interest from overseas investors remains robust. The country’s capacity for fresh milk and manufactured products has encouraged overseas manufacturers and investors to seek greater security by investing in the Australian industry, including farm aggregations.

While dairy commodity prices drive milk prices in southern Australia, the diversity of milk buyers has kept firm up ward pressure on farmgate prices. Processors buy milk on annual (or longer) contracts or agreements. In 2016, a retrospective step down in farmgate prices by two major processors sparked significant protest from the farm lobby into the nature and structure of milk supply contracts. The resulting loss of trust in the supply chain has exacerbated recent declines in milk supplies.

A government inquiry in 2016-17 led to a mandatory code of conduct for milk contracts. This code does not regulate prices but instead creates a standard set of requirements to improve the fairness and transparency of contracts for milk producers.

Moreover, with active derivative markets now offered in all of the major milk producing regions, producers have the opportunity to review forecast prices and arbitrage the difference between current and projected prices. Plus, buyers have the ability to forecast future costs from major supply regions.

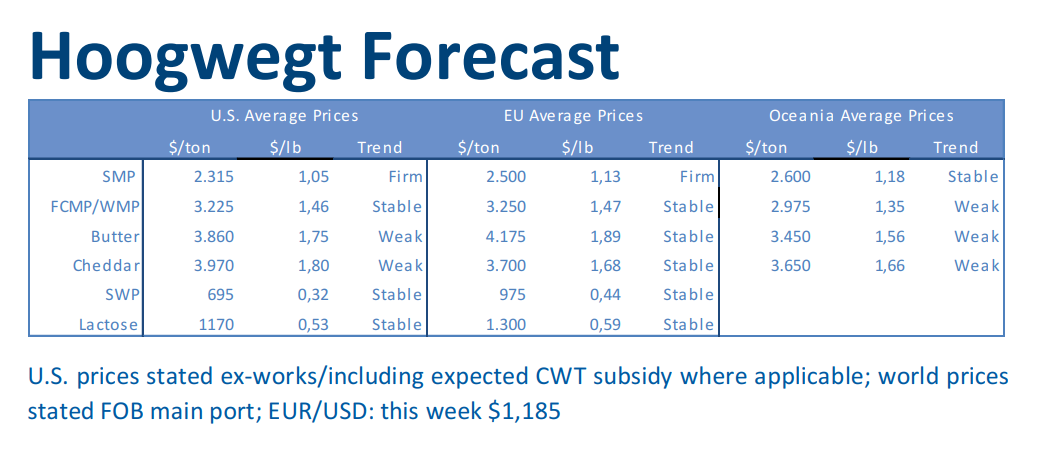

World Comment

During the first weeks of August it has been hot in the EU, putting the brakes on milk output for at least a short while. By now, weather conditions have normalized as well as production. Hence 2020 production growth is still expected to end up slightly above 1%. Oceania output is expected to be in line with 2019, mainly because of the strong second half of 2019 in New Zealand. Australia has started this new season well, and is expected to see solid growth rates in the months to come. The US is performing in line with earlier expectations. California can change this outlook, but so far it’s developing as expected.

On the demand side situation seems to be less impacted by Covid19 than initially assumed. April and May imports of the 10 largest importers have been ok compared to last year’s imports. Algeria’s May imports where better than May’19. And Mexico is performing now better than the start of 2020. In YTD terms Mexico is still effecting total trade growth negatively. China’s imports are becoming less strong. The high import figures does not seem to hold, resulting in about 6% less imports in June compared to last year.

Australian Output Making a Comeback

After a horrible start to 2020, which included scorching temperatures and the worst wildfires in Australia’s history caused by the Indian Ocean Dipole, a dramatic turnaround in weather,including widespread rainfall, has occurred. The climatic pattern has quickly shifted toward a cooler and wetter system in the southern regions of the country. However, most regions along the east coast remain in the grip of dry weather.

New milk contracting arrangements took effect in June, an acutely challenging time for processors juggling market uncertainty, increased competition, and a resurgence in the milk supply. Recent shifts in commodity markets and currencies have since weakened spot milk values for dairy commodities.

Despite the expectation that season over season milk prices will be close to 10% lower than in the 2019-20 season, dairy producer margins for the current season in Australia’s southern regions are expected to be favorable due to excellent pasture conditions and reduced grain costs. For the 2020-21 season, Dairy Australia expects milk output to grow 13% over the previous season.

Milk collections in southern regions in the four months to May 2020, were 10% higher than the prior year, although milk in northern regions, which produce for the fresh milk market,continued to contract. This has drawn more milk out of Northern Victoria, complicating the competition for milk in that region.

COVID19 has brought changes to Australia’s dairy markets similar to those seen elsewhere, including strong retail demand and a collapse in formal dining. A troubling second wave of COVID 19, which could dwarf first wave infections, threatens to force governments to impose longer restrictions. Rising geopolitical tensions with Australia’s major export market is a further troubling development that adds to market uncertainty.