MENA Market Struggles to Improve

Hoogwegt Horizon February 2020

The Middle East and North Africa (MENA) region, with a population of close to 430 million, is a major contiguous economic region with a high dependence on oil. In 2019, the region’s combined per capita gross domestic product (GDP) was$8,063 (U.S.), but at a country level, there is a wide range of prosperity. For example, the United Arab Emirates (UAE) per capita GDP last year was $37,750, Saudi Arabia’s was $22,865,and Egypt’s came in at $3,046, according to the International Monetary Fund (IMF).The region is one of the world’s largest dairy import markets,representing 19% of global exports in milk equivalents from the top12 dairy exporters over the 12 months to November 2019,including whole milk powder (WMP), skim milk powder (SMP),fatfilled milk powder and mixtures, and cheese.Local milk production generally provides a small portion of regional milk supplies, although this also varies. Some countries,such as Saudi Arabia, have made significant investments toimprove fresh milk availability for beverages and perishable dairy foods.

Impact of Weaker Crude Oil

The region’s economies have weakened significantly since an over supply of crude oil drove prices dramatically lower in 2014. A reduction in crude oil production made by the Organization of Petroleum Exporting Countries (OPEC) in 2017 in an effort to improve prices has hampered the region’s slow economic recovery. Most major oil producers in the region are members of OPEC. According to the IMF, GDP per capita across the MENA region fell 15.5% between 2013 and 2016, measured in U.S.dollars. While GDP has since recovered somewhat, the IMF estimates that at the end of 2019, the region’s GDP was still 8.5%below 2013’s level.Pressures on individual economies in the region have varied depending on an economy’s relative exposure to oil revenues and their impact on government reserves and consumer spending.The impact on businesses and consumers has varied further based on the use of consumer subsidies to cushion any economic effects.

Due to these household supports, the impact on average incomes has been less dramatic. The World Bank estimates that per capitai ncomes across MENA have grown at less than 1% per year over the five years since 2013. High inflation, which averaged more than 7% per year since 2013, has savagely eroded that small gain in income.

As a result of these pressures, the region’s imports of dairy products have grown at a much slower pace in recent years than expansion in global trade. After a rebound in imports of almost 30% in 2014 due to a retreat in dairy prices, the moving average annual rate of dairy trade to the region, in milk equivalents, has grown by just 2% from the end of 2014 through November 2019,whereas global dairy trade expanded 15% over that same period.Given the acute pressures on cost of living, dairy imports have been remarkably resilient, helped by population growth, which has expanded 11% since 2014.

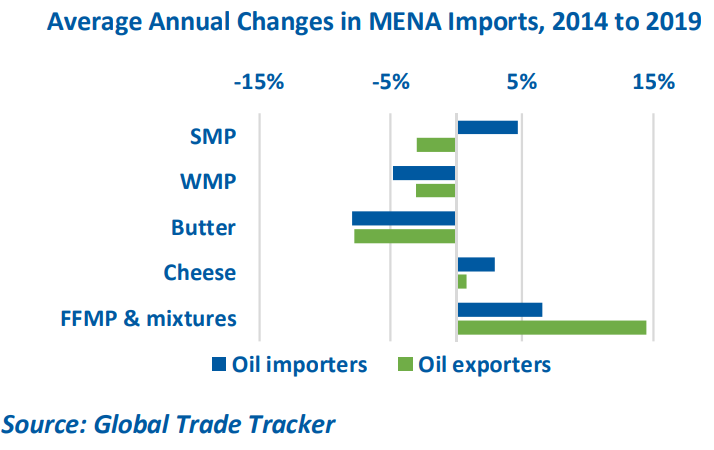

Over the past several years, an apparent “trading down” by consumers has been evident by the change in the composition of dairy trade to the region. Imports of butterfat have fallen by more than a quarter since 2014. Overall demand for milk powders has increased, but demand for WMP has been offset, in part, by increased consumption of fat filled milk powders in major Middle East markets, predominantly Saudi Arabia and the UAE, as manufacturers have taken advantage of less costly vegetable oils.

World Comment

The news that is clearly dominating the dairy market is the spread of the Corona virus.At the moment of writing this, Corona has spread into Europe. If the Corona virus wasn’t there we would have been discussing that the weak milk supply growth is keeping the market balance tight. The dry conditions on the Northern Island in New Zealand could become the next challenge for global supply. Rainfall has been very limited in the past days/week, so this could put an early end to an already challenging Oceania season. In Q2 supply growth in the West EU countries will increase to levels close to 1.5% but mainly because we are comparing with Q2 of 2019 when supply growth was still about 0%.General expectations are that supply will not strongly increase in H2 2020. Main reason is that there does not seem to be much appetite for investments and expansion. If we take the EU as an example we can conclude from recent history that the current milk price levels are no longer sufficient to incentivize stronger growth. This said, in the short run one issue will control the news, the Corona virus.

MENA to Remain Price Sensitive in 2020

The World Bank expects the combined GDP of the MENA region’s economies to grow by 2.4% in 2020, after growing just 0.1% in 2019, assuming little improvement in crude oil prices and stabilization in Iran following sanctions. Despite the expected slow improvement in crude oil prices in 2020, MENA’s oil exporters, as a group, aren’t expected to fare as well as the region as a whole, growing just 2%. At the same time, the GDP of the region’s oil importers is expected to increase by more than 4%, but these outlooks will depend on limited interruption from geopolitical conflicts.

MENA’s dairy imports improved in late 2019 as butterfat prices became more attractive, and Middle East demand for milk powders increased as EU stocks of SMP cleared the market.North Africa’s demand for SMP and WMP was much weaker than the Middle East’s due to significantly reduced purchases from Algeria. The austerity measures applied to curb consumer subsidies in Algeria could further limit milk powder imports by private buyers, and the economic and policy situation in Algeria remains uncertain.That said, overall milk powder (SMP) imports in the region have recovered to 2014 levels, and cheese imports have been even more resilient due to their access to retail outlets servicing affluent consumers. The region’s cheese imports were marginally better in 2019, compared to 2014 levels.Despite a better economic outlook, consumers and dairy commodity buyers across the region will likely remain sensitive to price due to continuing pressures on cost of living. The gradual erosion in WMP imports in favor of fat filled milk powder will continue, but the strength of ongoing import demand in 2020 for butterfat and cheese will be highly dependent on prices, which will be driven by supply and demand in other regions.