Can Demand Absorb Added Cheese Capacity?

Cheese dominates milk use and dairy consumption in most of the major dairy-exporting regions. Across the top-12 dairy exporters—the European Union, United States, Oceania, Latin America, and the Commonwealth of Independent States—about 46% of milk collections are processed into cheese. In the largest two producers, the European Union and the United States, cheese accounts for about 55% of milk use. Cheese consumption is increasingly important to balance milk supply and demand. Given declining fluid milk consumption, the volumes of milk available for manufacturing are expanding at a rapid rate in the major dairy-producing regions. To absorb expanding manufacturing milk supplies and service growing markets, major milk-producing countries in the European Union, Oceania, and the United States have steadily added cheese processing capacity over the past three years. More expansions are scheduled to come online through 2022. With potential for expansion in fast-food restaurants, much of the added capacity will be for mozzarella, especially in Europe and Oceania.

Gains in Cheese Demand Slowing

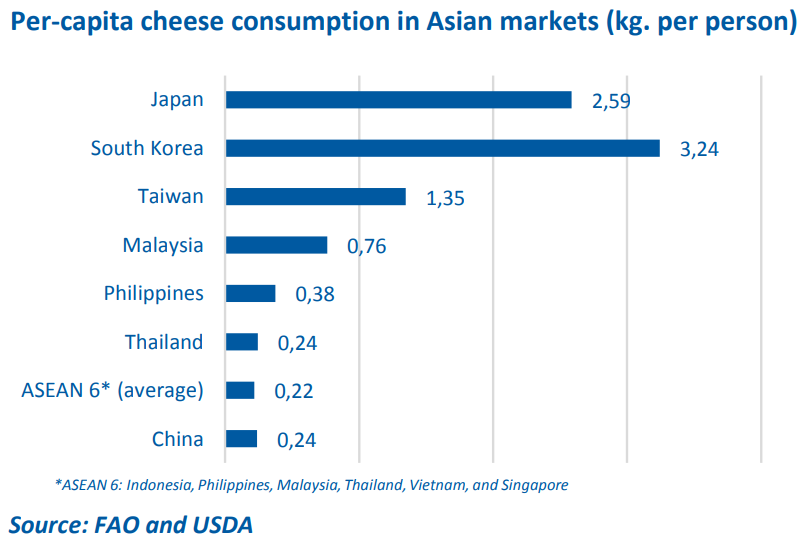

Domestic cheese demand in Europe and the United States has been expanding steadily. While the European Commission estimates that domestic cheese sales have slowed since 2017, demand has still grown at a rate of 2% per year over the five years to 2018. USDA estimates demand in the U.S. market has grown even faster, averaging 3.2% increases per year, twice the rate of the preceding five years, but U.S. growth waned in 2019. In the top-12 dairy exporters, only 9% of cheese output was exported and trade grew by just 1.6% per year in the five years to 2018. Excluding shrinkage in Russian imports, growth in other markets averaged more than 5% per year over the five years. Growth in cheese exports has been broad, spread across Japan, China, Southeast Asia, the Middle East, South Korea, and Australia. Developing markets, in particular, have offered exporters tantalizing opportunities given expansion in foodservice and modern retail networks.

Japan’s imports increased the most over the five-year period to 2018, despite its stagnant population and sluggish economy. Innovations in snack foods and fast-food options have expanded cheese-eating occasions in Japan. South Korea’s demand for mozzarella has grown with greater acceptance of fast food, while demand in Southeast Asia and China has also expanded as tastes there have developed.

If per-capita consumption of cheese were to follow the trends seen in other dairy categories, such as yogurts and beverages, enormous upside potential would exist in these markets. While China’s per-capita consumption of cheese is lower than Japan’s, the natural cheese market in China, a country with more than 11 times the population of Japan, is already slightly larger. Competition among major exporters to serve this expanding demand has been intense. The European Union has gained the most market share since 2015 as it dealt with loss of access to the Russian market and elimination of milk quotas. The European Union has also benefitted from a prodigious use of free trade agreements and geographical indications to build access in expanding markets, helping it grow exports by 16% in the three years to 2018, while the world market grew by 10%.

World Comment

Most recent statistics show a modest milk production increase in USA, stable numbers in EU and a decrease in Oceania; mainly caused by unfavorable weather during the start of the season. The additional milk in USA mainly flew to cheese production. European butter prices have recovered after recently reaching its 3 year lowest point, 2019 exports year to date are 28% higher than last year and prices are likely to go above Oceania levels again soon. Skim Milk Powder is still bullish; in the last 12months prices have increased about 50% and general level has reached USD3000/Mt CFr, which could be a psychological barrier. Whereas the milk valorization is often in favor of cheese, some producers in the EU indicate that producing butter and SMP gives a better valorization today, leading to higher cheese prices. Interesting factor to follow closely in the coming period is the additional Mozzarella capacity that will come online. For sure it will absorb a lot of milk. During this weeks’ GDT, the cheddar price went up, bringing it on par with EU cheddar. Since the US prices are still high, the demand from the world market will be fulfilled by either Oceania or the EU. Fundamental supply and demand balance is not likely to change in coming months, so it seems logical that general bullish sentiment will continue.

Global Cheese Trade Could Slow in 2020

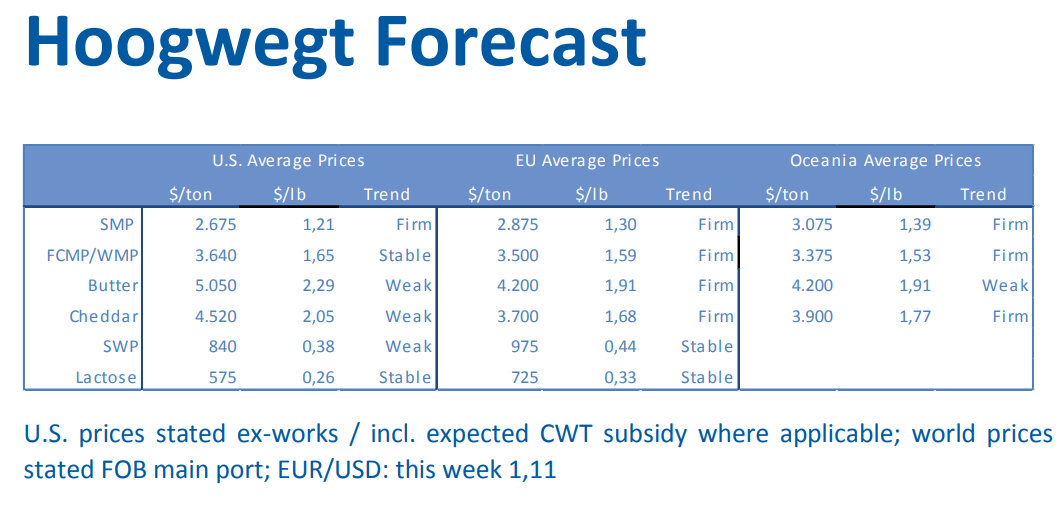

After slowing growth in global cheese trade in 2018, activity has picked up. Cheese trade increased 3.2% in the first eight months of 2019. Excluding shipments of cheese from Belarus to Russia, however, trade into all other markets grew at about half that pace. Meanwhile, wholesale cheese prices in the European Union and the United States have dramatically diverged. EU cheese supplies are currently abundant given increased capacity, while tight U.S. cheddar supplies have driven U.S. prices higher. However, as output improves and consumers respond to higher prices, U.S. prices will retreat. In the short-term, EU exporters will maintain their price advantage. Policy headwinds in the coming year threaten cheese market growth. Eventual agreements regarding Brexit could weaken the UK cheese market (the largest single market in Europe after its exit from the European Union) or eventually reduce access for EU producers. Early signals suggest UK producers could be harmed if the United Kingdom were to sign a non-EU trade deal that sets import tariffs lower than those that currently apply to EU cheeses. A further slowing of trade is likely with the imposition of U.S. tariffs on EU cheese imports, arising from the World Trade Organization’s decision on illegal EU airline subsidies. Moreover, the chance of a global recession occurring next year increases without resolution of the U.S.-China trade dispute, which would also contribute to a slowing of cheese trade in 2022. Increased cheese supply will add further downward pressure on prices. Significant additional production capacity will come online next year. While major plant additions in the United States have mostly focused on cheddar, in the European Union, the emphasis has been on mozzarella. Global mozzarella prices are already being pressured by abundant supplies, so it will take a major lift in demand to keep world markets balanced. $/ton $/lb Trend $/ton $/lb Trend $/ton $/lb Trend SMP 2.675 1,21 Firm 2.875 1,30 Firm 3.075 1,39 Firm FCMP/WMP 3.640 1,65 Stable 3.500 1,59 Firm 3.375 1,53 Firm Butter 5.050 2,29 Weak 4.200 1,91 Firm 4.200 1,91 Weak Cheddar 4.520 2,05 Weak 3.700 1,68 Firm 3.900 1,77 Firm SWP 840 0,38 Weak 975 0,44 Stable Lactose 575 0,26 Stable 725 0,33 Stable U.S. Average Prices EU Average Prices Oceania Average Prices Did You Know? The expansion of EU mozzarella capacity is expected to add about 250,000 metric tons (MT) of output from 2018 through 2020. A single U.S. cheddar plant proposed in Michigan will add about 135,000 MT of capacity in late 2020. The European Union captured 60% of the growth in combined exports from the top-12 dairy exporters between 2015 and 2018, while the United States gained 17% and New Zealand suffered a 3% loss. If Chinese per-capita consumption were to expand to equal that of Taiwan, China would need to import or make an additional 1.6 million MT of cheese.