Algeria Faces Challenges Going Forward

hoogwegt april 2019 horizon

Algeria is a vital dairy market facing serious internal and external challenges as it spends to keep dairy and other food staples affordable to consumers at the same time fiscal reserves have been severely depleted due to slumping oil revenues.

Last year, Algeria was the third largest dairy importing country after China and Mexico, according to estimates based on exporters’ reported data. Algeria had a population of 41 million in 2017, with a GDP of $4,055 (U.S.) per capita, according to the World Bank. Estimated annual percapita dairy consumption was 114 liters (milk equivalents), the highest in Africa, while dairy represented about 8% of average household food expenditures, according to a 2017 study by the Algerian Association of Beverage Producers. In 2018, dairy represented about 16% of Algeria’s food imports by value.

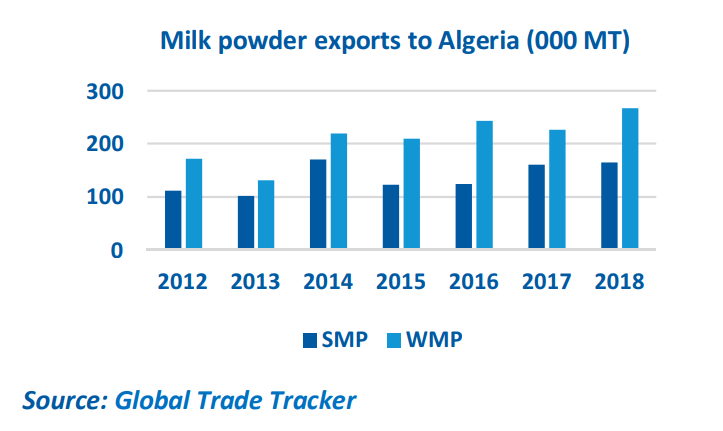

Milk drinks made from reconstituted milk powders dominate the country’s dairy consumption, making Algeria a significant market for whole milk powder (WMP) and skim milk powder (SMP). However, the fresh milk market and demand for cheese, yogurts, and dairybased desserts are growing. In an effort to address dairy product shortages—despite a weaker fiscal position— Algeria imported 267,000 metric tons (MT) of WMP and 165,000 MT of SMP in 2018, both significantly higher than the averages over the previous four years. While the European Union typically dominates SMP trade to Algeria, exporters in New Zealand, Latin America, and Europe share the WMP market.

Import tariffs of 5% apply to milk powders, but tariffs increase to 30% for cheese. Dairy imports are tightly regulated and procured by a mix of licensed private buyers and the Office National Interprofessional du Lait (ONIL), the government purchasing agency, which accounts for 4050% of imports. ONIL periodically calls for large tenders of milk powders.

Dairy sector policy

The Algerian economy is highly dependent on revenues from the oil and natural gas industries, which represent about 20% of GDP and 95% of merchandise exports, mostly supplied to the European Union. Since 2014, oil prices have remained below the country’s breakeven point, and recent OPECmandated production cuts have weakened government revenues and placed fiscal pressure on the country’s food policies and programs.

The Algerian government aims to reduce all dairy imports, through import controls and expansion of local milk production. In January 2018, dairy import regulations changed, requiring importers to be licensed using a system of shortterm licenses. The age of products that can be imported is also limited to three months for shipments that originate in the European Union and four months for product sourced elsewhere. Milk powder exports to Algeria (000 MT) Source: Global Trade Tracker

In May 2018, Algeria issued a temporary import ban on a wide range of food products, but the government has not placed a ban on dairy product imports. Despite Algeria’s policy objectives, the country’s milk powder imports increased 11% in 2018.

The government has an ambitious plan to expand local milk production 50% by increasing yields per cow to 6,000 liters (13,623 lbs.) over two years, which will require imported genetics and livestock. In 2017, Algeria’s 971,000 milk cows produced about 2.6 billion liters (5.9 billion pounds) of milk, putting average production per cow at 2,700 liters (6,134 lbs.). The government also provides subsidies to milk producers, processors, and distributors of fresh and ultrahigh temperature (UHT) milk to reduce reliance on reconstituted milk drinks and fix consumer prices at affordable levels.

World Comment

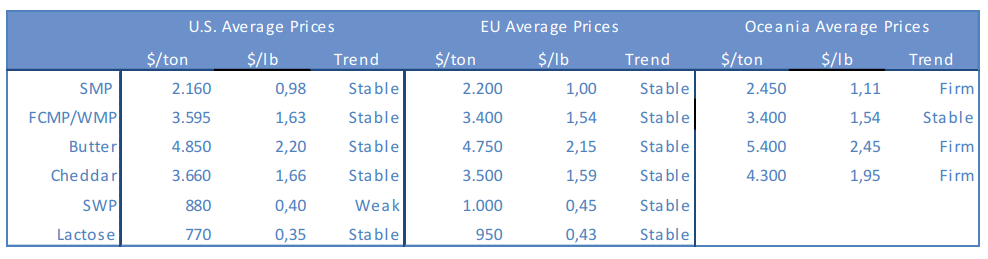

Milk production in the world is not convincing in most regions, the season in the Southern Hemisphere is winding down and the first 2 months of 2019 in US and Europe are not very strong either; whereas the main producing European countries Poland, Ireland and Belgium are showing a yearonyear increase, total EU28 milk production is showing at 1.6% decrease compared to last year. Reasons for lower production vary from phosphate regulation issues in The Netherlands to farm economics in, for example, France. Of course flush is yet to start so things can change quickly in coming weeks / months. Although milk production is not looking promising it seems buyers remain comfortable and are absolutely not in a hurry to cover any further forward than normal. SMP prices have been moving sideways for a couple of weeks now and market, although thinly traded, feels balanced. However this can change quickly if for example big markets like Mexico for US NFDM or Algeria for EU SMP become more active again. China imports have been strong first months of this year and are expected to remain so. The prices of most other commodities are fairly stable as well, only New Zealand fat is trading well above the rest of the world. In a few weeks we will have a better idea how the supply and demand balance will develop and what prices we will see in coming months.

Outlook for Algeria Remains Fragile

Despite Algeria’s policy objective to reduce dairy product imports, low WMP and SMP prices provided ONIL with an incentive to build stocks in 2018. Market share of Algeria’s WMP imports changed significantly as Uruguay and Argentina took advantage of their weak currencies to more than double their previous market share, largely at the European Union’s expense.

WMP trade to Algeria could slow in 2019, at least in for the short term, now that firmer ingredient prices prevail and global supplies have tightened.

Algeria’s fragile economic outlook provides a further challenge that will continue to evolve. Continuing weakness in oil revenues and expanded public spending, designed to keep the costs of staple goods and services affordable, have been pushing the government into a spiraling fiscal deficit. Not only is Algeria’s trade deficit growing, but the country’s falling export earnings could also further impact ONIL’s ability to purchase dairy imports. The country also plunged into political crisis due to weeks of large, peaceful protests, which were eventually followed by a change in leadership ahead of the upcoming elections. The rate of inflation has climbed to more than 6% and will increase further in 2019, adding to societal tension. Improving oil prices could gradually lift the country’s trade out of its perilous state, but the changing dynamics of the global oil market will continue to put pressure on fiscal reserves. However, Algeria has a long history of stability, which its leadership will strive—and spend—to preserve. Economic reform in the country is inevitable if Algeria is to maintain its important place in the global dairy market.